The 5 Sub-Sectors of Indian AgriTech Where European Innovation Wins

India’s AgriTech market is entering a different phase.

The first decade was dominated by digital aggregation — marketplaces, lending platforms, and farm apps competing for scale. The next decade will be defined by infrastructure, climate resilience, biological productivity, and operational efficiency.

For European AgriTech founders, this shift creates a major opportunity — but only in specific categories.

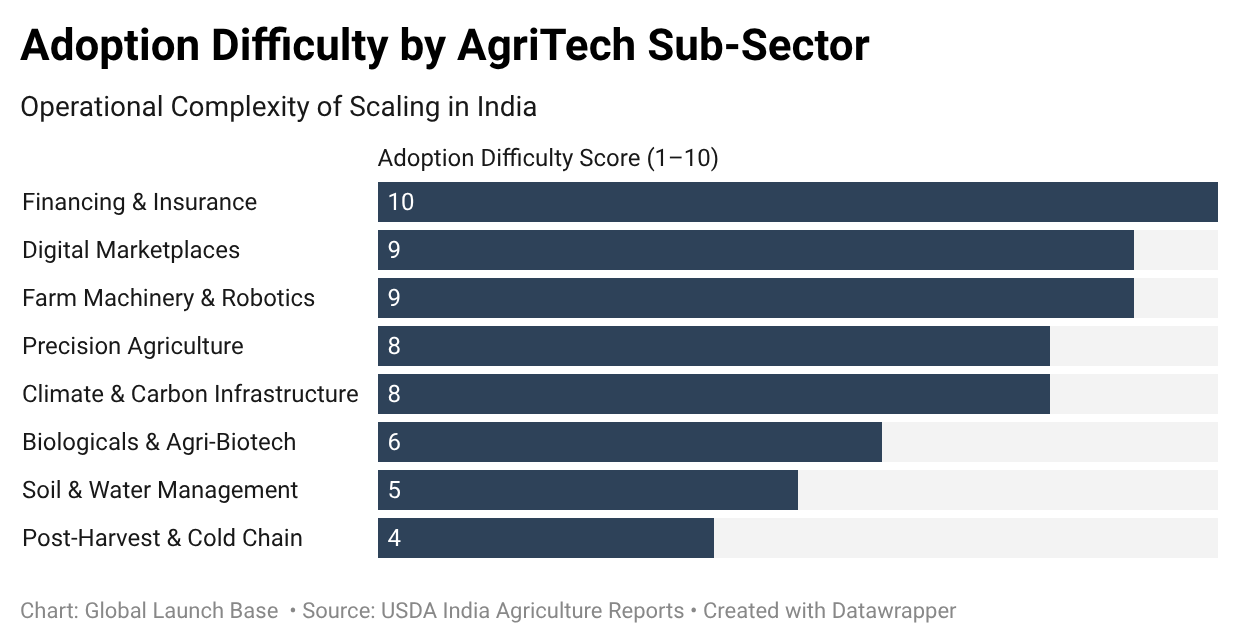

Many European startups enter India assuming that strong technology alone guarantees adoption. In reality, Indian agriculture operates under a very different set of constraints: fragmented landholdings, price-sensitive farmers, uneven infrastructure, extreme climate variability, and highly localized cropping systems.

Some sub-sectors align exceptionally well with European strengths in engineering, sustainability, automation, and agricultural science. Others are brutally difficult unless companies localize deeply from day one.

At Global Launch Base and the broader DutchBaseCamp ecosystem, this distinction matters. European founders need to know where India is ready for international innovation — and where the market will resist imported models.

This article maps eight major Indian AgriTech sub-sectors across two dimensions:

- European Competitive Advantage

- Indian Market Readiness

The result is a practical framework for where European innovation is most likely to succeed.

The New Structure of Indian AgriTech

Indian AgriTech is no longer a single category.

The market has fragmented into multiple ecosystems with different economics, adoption cycles, regulatory barriers, and infrastructure needs.

The eight sub-sectors shaping the next phase are:

- Precision Agriculture

- Biologicals & Agri-Biotech

- Post-Harvest & Cold Chain

- Farm Machinery & Robotics

- Digital Marketplaces

- Agri Financing & Insurance

- Soil & Water Management

- Climate, Carbon & Sustainability Infrastructure

Each category behaves differently in India — and European companies are not equally positioned across them.

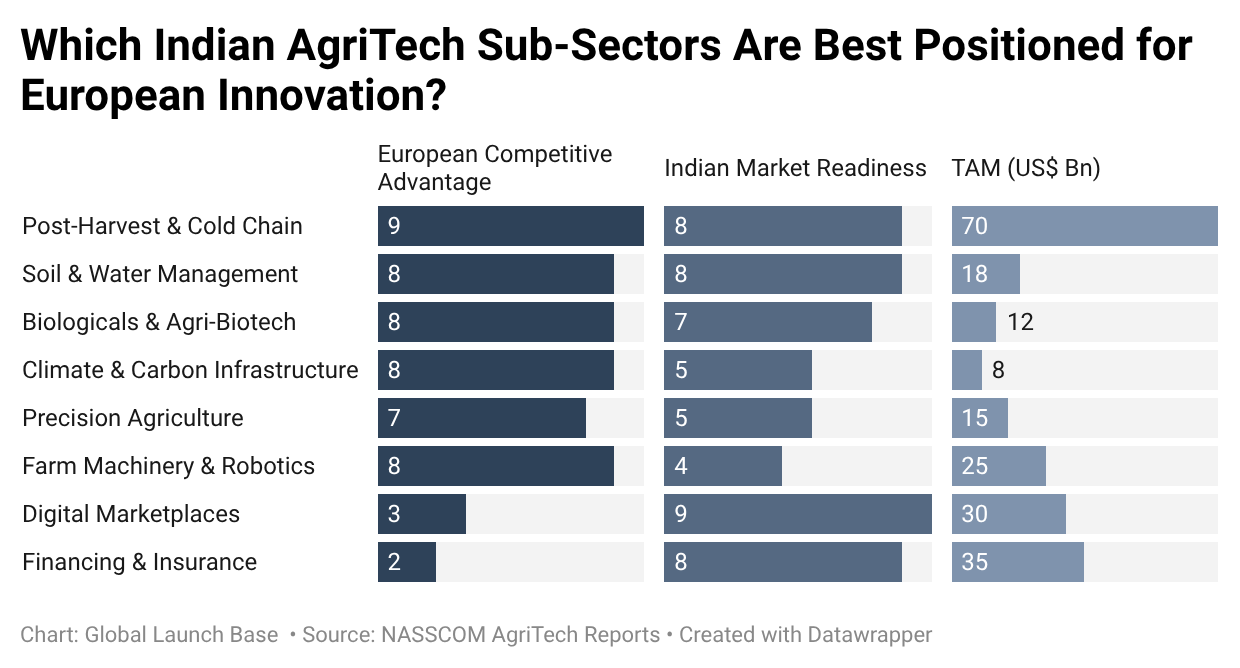

The Framework: Where European Innovation Fits

The proposed 2×2 matrix evaluates each sub-sector on:

Sub-Sector | European Competitive Advantage | Indian Market Readiness | Indicative Outcome |

|---|---|---|---|

Post-Harvest & Cold Chain | Very High | High | Invest Now |

Soil & Water Management | High | High | Invest Now |

Biologicals & Agri-Biotech | High | Medium-High | Invest Now |

Climate & Carbon Infrastructure | High | Medium | Monitor / Early Entry |

Precision Agriculture | Medium-High | Medium | Build Local First |

Farm Machinery & Robotics | High | Low-Medium | Build Local First |

Financing & Insurance | Low | High | Avoid |

Digital Marketplaces | Low | Very High but Saturated | Avoid |

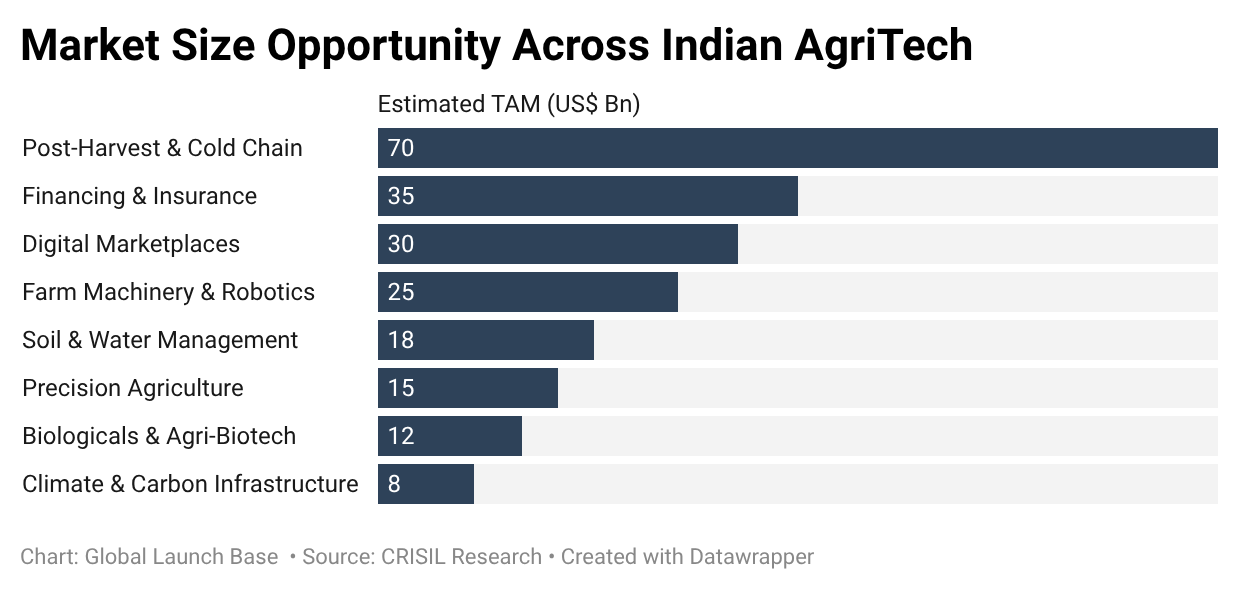

Bubble size in the final matrix can represent total addressable market (TAM), with post-harvest infrastructure, financing, and marketplaces representing the largest opportunity pools.

1. Post-Harvest & Cold Chain

Why European Companies Win Here

This is arguably the strongest fit between European capability and Indian demand.

India loses enormous agricultural value after harvest due to weak cold storage, fragmented logistics, inconsistent grading, and inadequate processing infrastructure. Fruits, vegetables, dairy, fisheries, and floriculture are especially affected.

European firms bring decades of expertise in:

- Controlled atmosphere storage

- Refrigeration systems

- Food traceability

- Packhouse automation

- Cold logistics optimization

- Quality grading systems

- Energy-efficient storage

Indian demand is now catching up quickly due to:

- Growth in organized retail

- Export-oriented agriculture

- Food processing expansion

- Q-commerce grocery networks

- Government infrastructure incentives

This sector also aligns well with state-level subsidy programs and institutional financing.

Unlike purely digital AgriTech models, post-harvest infrastructure solves a visible economic pain point with measurable ROI.

For European founders, this is one of the clearest “Invest Now” categories.

2. Soil & Water Management

Europe’s Sustainability Expertise Matches India’s Urgency

India’s agricultural future depends heavily on water efficiency.

Groundwater depletion, erratic monsoons, salinity, declining soil quality, and fertilizer imbalance are becoming structural risks across multiple states.

European companies have strong capabilities in:

- Precision irrigation

- Water monitoring systems

- Soil sensing

- Nutrient optimization

- Controlled fertigation

- Greenhouse water efficiency

- Regenerative agriculture systems

Indian readiness is rising because farmers increasingly understand the economic impact of water scarcity.

Government support for micro-irrigation, watershed development, and climate adaptation further strengthens the category.

The strongest opportunities are likely in:

- Horticulture clusters

- Export-oriented farming

- Plantation agriculture

- Greenhouse cultivation

- High-value crops

This is particularly relevant for regions transitioning toward climate-resilient farming systems.

3. Biologicals & Agri-Biotech

A High-Potential Category With Long-Term Tailwinds

India is gradually shifting toward biological agriculture inputs.

The transition is not ideological — it is economic.

Rising fertilizer costs, pesticide resistance, export residue restrictions, and soil degradation are pushing growers toward:

- Bio-stimulants

- Bio-fertilizers

- Microbial formulations

- Biological pest control

- Sustainable crop protection

European firms possess deep research capabilities and regulatory experience in biological agriculture.

However, Indian adoption still depends heavily on:

- Demonstration farming

- Extension services

- Distributor trust

- Region-specific validation

This is not a “sell software remotely” market.

Companies that succeed usually combine technology with local agronomy partnerships and field-level validation networks.

Institutional collaboration with organizations such as ICAR-CPCRI and regional agricultural universities can significantly improve adoption credibility.

4. Climate & Carbon Infrastructure

Large Future Potential — But India Is Still Early

Climate-focused agriculture is attracting global attention, but India remains in the early infrastructure phase.

The opportunity includes:

- Carbon measurement

- MRV systems

- Climate-resilient farming

- Carbon credit aggregation

- Nature-based agriculture

- Regenerative verification systems

European companies often lead in sustainability frameworks, carbon accounting methodologies, and environmental compliance systems.

But several constraints remain:

- Fragmented land ownership

- Smallholder verification complexity

- Unclear carbon economics for farmers

- Limited standardization

- Policy uncertainty

The long-term potential is enormous, especially as food exporters face sustainability reporting pressure from Europe.

However, many climate-agriculture models in India are still searching for scalable economics.

This sector belongs in the “Monitor / Early Entry” quadrant rather than immediate aggressive expansion.

5. Precision Agriculture

Strong Technology, But Localization Is Everything

Precision agriculture is frequently misunderstood in India.

European systems built for large mechanized farms often struggle in smallholder environments where average farm sizes are dramatically smaller.

Still, opportunities exist in:

- Plantation crops

- High-value horticulture

- Greenhouses

- Export farms

- Corporate farming clusters

The challenge is not the technology itself.

The challenge is operational adaptation.

Indian agriculture requires:

- Ultra-low-cost deployment

- Offline functionality

- Multilingual interfaces

- Advisory integration

- Local agronomy models

- Dealer-led support systems

Drone-based agriculture is growing rapidly, but profitability remains inconsistent outside subsidy-supported deployments.

European firms entering this space usually need Indian channel partners and localized service layers before scaling becomes realistic.

6. Farm Machinery & Robotics

Advanced Engineering Meets Smallholder Reality

Europe has exceptional agricultural engineering capabilities.

India, however, remains one of the world’s most difficult environments for advanced farm robotics.

The main constraints are structural:

- Small fragmented farms

- Labor economics

- Mixed cropping patterns

- Terrain variability

- Limited service infrastructure

Large autonomous machinery models that work in Europe often fail commercially in India without redesign.

The strongest opportunities are not necessarily in full automation.

Instead, promising segments include:

- Small-scale mechanization

- Shared machinery platforms

- Orchard automation

- Precision spraying

- Lightweight electric equipment

- Robotics for protected cultivation

European companies that redesign products specifically for Indian farm conditions may succeed. Those attempting direct market transfer usually struggle.

7. Digital Marketplaces

The Market Is Already Crowded

India has already gone through a major AgriTech marketplace cycle.

Over the past decade, hundreds of startups attempted to digitize:

- Input distribution

- Produce trading

- Farm procurement

- B2B agri-commerce

Most faced the same challenge:

Agriculture is ultimately a logistics and trust business — not just a software business.

Indian startups already dominate this category because they understand:

- Regional supply chains

- Trader networks

- Rural credit behavior

- Last-mile operations

- Political and mandi dynamics

For European entrants, competitive advantage is weak unless combined with unique infrastructure or embedded financing.

This category is now heavily crowded and operationally demanding.

8. Financing & Insurance

A Difficult Sector for Foreign AgriTech Entrants

Agri-finance and insurance in India depend heavily on:

- Local credit behavior

- Government programs

- Banking relationships

- Rural collections

- Regulatory familiarity

- Embedded distribution

European firms generally lack structural advantages here.

Meanwhile, Indian fintechs and NBFCs already possess:

- Local data models

- Distribution networks

- Government integrations

- Risk understanding

Insurance penetration remains low, but the complexity of underwriting Indian agriculture makes the sector difficult for foreign startups without major local partnerships.

This is one of the weakest fit categories for direct European expansion.

Why Localization Matters More Than Technology

The biggest mistake international AgriTech companies make in India is assuming that technology adoption works like Europe.

It doesn’t.

Indian agricultural adoption is driven by:

- Demonstrated ROI

- Peer farmer influence

- Local language support

- On-ground agronomy trust

- Distributor relationships

- Service responsiveness

- Financing availability

Technology alone rarely scales without ecosystem integration.

That is why partnerships matter.

The most successful international AgriTech models in India usually involve:

- Local agronomy teams

- Research collaborations

- State-level pilots

- Farmer producer organizations (FPOs)

- Demonstration farms

- Infrastructure partnerships

Aré Guḍi as a Live Testbed

At Aré Guḍi in Karnataka, several of these themes are already visible in practice.

The farm serves as a live operational environment where questions around plantation efficiency, soil management, biodiversity, irrigation, climate adaptation, and agricultural infrastructure can be evaluated under real Indian farm conditions.

While still small in scale, such testbeds matter because they bridge the gap between laboratory innovation and field adoption — a gap that remains one of the defining challenges in Indian AgriTech.

Where European AgriTech Should Focus Next

For European founders evaluating India, the key lesson is simple:

India is not one AgriTech market.

Some sectors strongly reward European expertise. Others structurally favor deeply localized Indian operators.

The strongest near-term opportunities appear in:

- Post-harvest infrastructure

- Cold chain systems

- Water management

- Biological agriculture

- Sustainability infrastructure

The weakest fit areas are:

- Pure digital marketplaces

- Commodity agri-finance

- Generic platform models without operational depth

The winners in India’s next AgriTech cycle will likely be companies that combine European technology strengths with Indian operational realism.

That combination — not technology alone — is where durable advantage will emerge.